Why Two Identical Salaries Can Lead to Very Different Retirement Lifestyles

Many people spend their careers focused on reaching the next salary milestone or securing a promotion, but financial progress shouldn’t be measured by your paycheck alone. The decisions you make in your peak earning years are just as important as the size of your paycheck. One of the most significant risks is lifestyle creep, which is the tendency for everyday spending to rise alongside income. How you manage a salary raise today can have a significant impact on your long-term financial security. Without a strategy for handling salary increases, even a high-earning household can find themselves ill-prepared for the future.

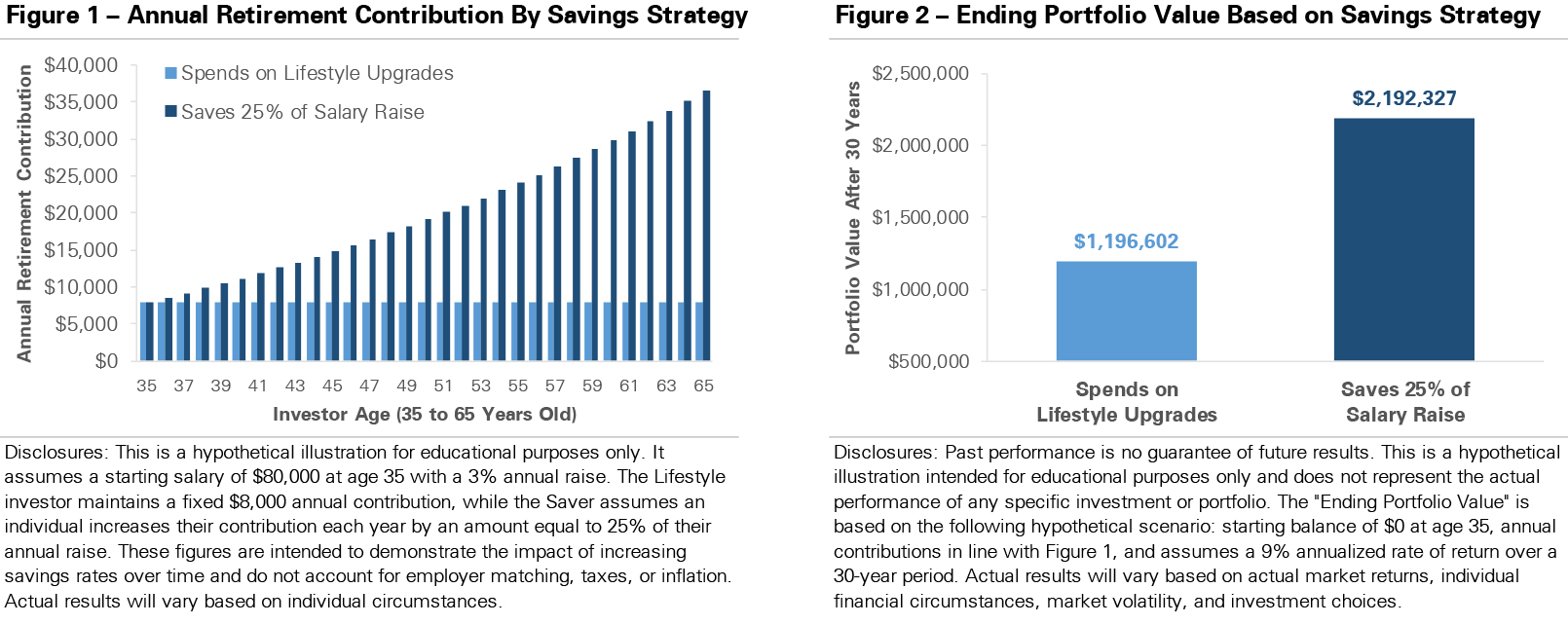

The charts below demonstrate how different approaches to a salary increase can impact a retirement portfolio’s growth. They are based on a hypothetical scenario: two individuals aged 35 make $80,000 annually and receive 3% annual raises. Both start by contributing 10% of their salary, or $8,000, to retirement savings. The two sets of bars in Figure 1 track different strategies for managing the raises and retirement contributions. The Lifestyle individual keeps their annual contribution fixed at $8,000. Every dollar of every raise is spent on immediate lifestyle upgrades, such as a nicer car, another trip, or higher discretionary spending. The Saver individual takes a more balanced approach, setting aside 25% of every raise while enjoying the rest. For example, a $2,000 raise would increase the next year’s contribution by $500, or 25%.

While both individuals earn the same amount, their retirement savings quickly diverge. Figure 2 graphs the ending portfolio values at age 65, reflecting 30 years of each individual’s savings strategy. These hypothetical ending account values assume the portfolios earn a +9% annual return. Over 30 years, the Lifestyle individual contributed nearly $250,000, which grew to nearly $1.2 million. The Saver individual contributed nearly $630,000, which grew to nearly $2.2 million, almost $1,000,000 larger than their peer’s. The difference isn’t just additional savings but decades of compounding that can extend a portfolio’s life in retirement or create the option to retire earlier. In contrast, the Lifestyle individual not only saves less but also increases their base cost of living, which will require a larger portfolio to sustain their lifestyle in retirement.

It is our belief that building long-term wealth isn’t just about what you earn; it’s about how you manage the surplus as you earn it. Raises can either disappear into lifestyle upgrades or become a powerful tool for future security and flexibility. It’s about finding a balance between enjoying the reward of hard work today and saving for your future. There is no one-size-fits-all approach, and the method you start with doesn’t have to be permanent. Everyone’s retirement looks different, and the right strategy depends on your goals and life stage. Our goal is to help you create a savings strategy tailored to your distinct needs and goals so that when the time comes, you are ready to enjoy retirement.

Important Disclosures

Published by Market Desk Research and distributed by QuadCap Wealth Management, LLC.

This client letter is being furnished by QuadCap Wealth Management, LLC (“QuadCap”) on a confidential basis for the exclusive use of clients of QuadCap. and may not be disseminated, communicated, reproduced, redistributed or otherwise disclosed by the recipient to any other person without the prior written consent of QuadCap.

This document does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services. Such an offer may only be made to prospective investors by means of delivery of an investment advisory agreement, subscription agreement and other similar materials that contain a description of the material terms relating to such investment, investment strategy or service. This presentation is being provided for general informational purposes only.

This presentation includes information based on data found in independent industry publications and other sources and is current as of the date of this presentation. Although we believe that the data is reliable, we have not sought, nor have we received, permission from any third-party to include their information in this presentation. Charts, tables and graphs contained in this document are not intended to be used to assist the reader in determining which securities to buy or sell or when to buy or sell securities. Opinions, estimates, and projections constitute the current judgment of QuadCap and are subject to change without notice.

References to any indices are for informational and general comparative purposes only. There are significant differences between such indices and the investment programs described in this presentation. References to indices do not suggest that the investment programs will, or are likely to, achieve returns, volatility, or other results similar to such indices. The performance data of various indices presented herein was current as of the date of the presentation.

Past performance is not indicative of future results and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable or equal any corresponding index or benchmark. The performance information shown herein is based on total returns with dividends reinvested and does not reflect the deduction of advisory and/or other fees normally incurred in the management of a portfolio.

Advisory Services are offered through QuadCap, an SEC registered investment advisor. QuadCap only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration is not an endorsement of the firm by the Commission and does not mean that QuadCap has attained a specific level of skill or ability.