4Q 2025 Recap & 1Q 2026 Outlook

Key Updates on the Economy & Markets

Markets navigated a complex environment in Q4. The quarter started with a government shutdown, which lasted 43 days and delayed key economic data releases. The lack of timely information made it difficult to assess the economy’s strength and contributed to periods of volatility as the market reacted to incomplete information. The Fed cut interest rates by -0.50% but signaled a pause, hinting that it could cut less than the market expects in 2026. Investors remain excited about the potential of artificial intelligence, but they’ve become more focused on which companies are best positioned to turn AI demand into near-term profits. Against this backdrop, the S&P 500, Nasdaq, and small-cap stocks each set new highs. In this letter, we recap Q4’s defining themes and events, review performance across key market areas, and look ahead to 2026.

Government Shutdown Creates a Data Fog

The main story in Q4 was the government shutdown and its impact on economic visibility. The shutdown started on October 1st and immediately disrupted the release of key reports on employment, inflation, and growth. To fill the data gap, the market and economists turned to corporate earnings reports and surveys from non-government sources. The shutdown lasted through mid-November, making it the longest in history, and it left behind a data backlog that is still being cleared as the new year begins.

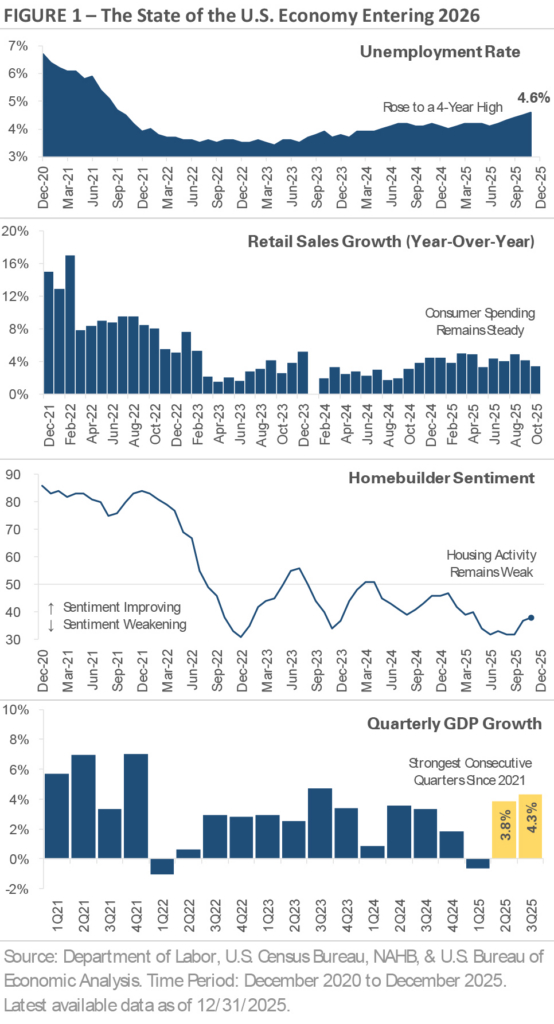

The stacked charts in Figure 1 provide an update on the economy using labor, consumer spending, and housing data released after the shutdown. The top chart shows labor market conditions continued to soften in Q4, with unemployment rising to a four-year high as hiring slowed. The second chart, which graphs the year-over-year growth rate of retail sales, highlights the consumer’s resilience. Consumer spending has cooled since 2022, but it remains steady despite affordability challenges and persistent inflation. The third chart graphs the homebuilder sentiment index, where readings above 50 signal positive sentiment. The index ticked higher in recent months, but it remains below 50, an indication that housing activity continues to run below the pre-pandemic trend. The bottom chart shows GDP growth rose to +4.3% in Q3, up from Q2’s +3.8%. Those are the strongest consecutive quarters of growth since 2021, before the Fed’s aggressive rate hiking cycle.

The data reveal a late-cycle economy that is slowing but not breaking. Labor market conditions are soft, consumer spending is slowing, and housing is under pressure, but the economy shows few signs of significant stress. The strong Q3 GDP reading indicates the economy reaccelerated after slowing in Q1, suggesting consumers and businesses altered their behavior in 2025 due to shifting trade policy and tariffs. Now that the trade policy uncertainty has eased, there’s a debate about where economic activity will settle in 2026. The uncertainty explains the Fed’s cautious tone and the market’s heightened sensitivity to new data.

Fed Cuts Twice but Signals a Pause in Early 2026

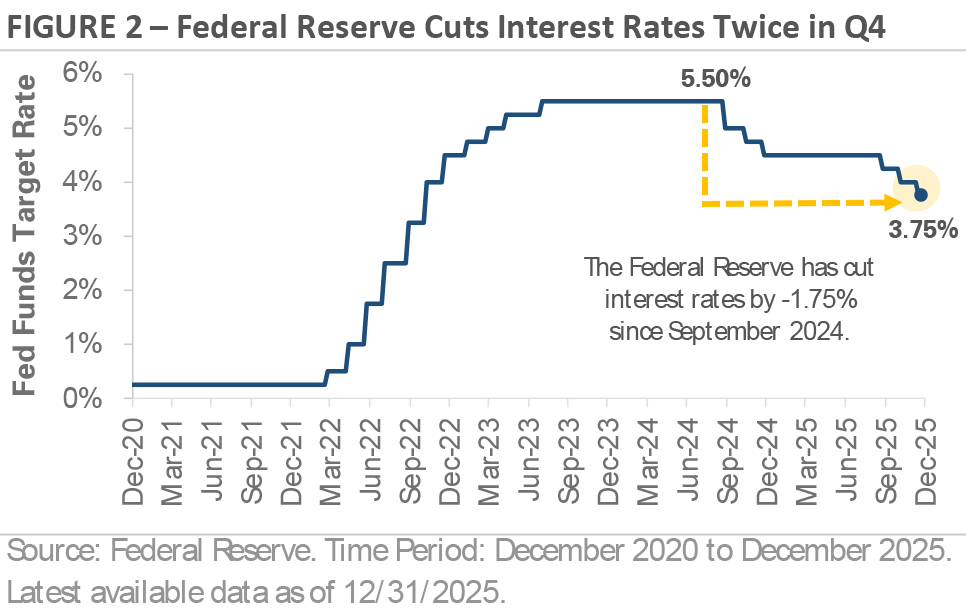

The Federal Reserve continued its rate-cutting cycle in Q4, but policymakers delivered a more nuanced message than simply lowering rates and offering forward guidance. Figure 2 shows the Fed has cut interest rates by a total of -1.75% since starting its rate-cutting cycle in September 2024. Two of those cuts came in Q4, with -0.25% reductions at the October and December meetings. However, the messaging behind the two cuts changed. Officials have grown more cautious and divided, with several voting members favoring either no cut or a larger cut, and they’ve emphasized that future rate cuts will depend on incoming data.

Uncertainty around Fed policy led to wide swings in market expectations. Investors flipped between pricing in multiple rate cuts and a slower, cautious rate-cutting cycle. Fed officials themselves appeared divided, with some warning that policy remains too restrictive and risks slowing economic growth while others caution that cutting too soon could reignite inflation. The shutdown added to the confusion by delaying key economic data, making Fed policy a source of near-term uncertainty and market volatility.

The question is what happens next. By quarter-end, Fed officials made clear that the threshold for additional rate hikes is high, but they also stressed the need for flexibility and patience. The current backdrop is a mix of cooling inflation, a soft labor market, and a still-expanding economy. Looking at Figure 2, the setup is similar to late 2024, when the Fed cut multiple times before pausing for nine months. This time it’s the shutdown data fog making it difficult for the Fed to forecast policy. The Fed has signaled that it will pause in early 2026 and potentially cut fewer times than the market expects. The prospect of additional rate cuts and lower interest rates is supportive in principle, but the policy outlook is now more sensitive to incoming data. That sensitivity contributed to the Q4 stock market volatility, and it will likely remain a market driver in early 2026.

The AI Trade Becomes More Selective

Artificial intelligence remained a key investment theme in Q4, but the narrative matured. AI stocks entered the quarter with strong momentum, powered by robust earnings, a boom in data center construction, and a growing list of large-scale infrastructure investment projects. Investors were optimistic that AI capex would translate into growth and increased profitability, and many AI-related stocks benefited from broad enthusiasm toward the industry.

Midway through the quarter, the market’s focus shifted. Earnings reports continued to signal strong demand for AI-related computing power and data centers, and leading tech companies reported large, growing backlogs. However, investors started to look beyond headline growth and focus on AI’s economics. Questions emerged about the capital needed to build and maintain data centers, the impact of aggressive capex spending on balance sheets, and whether companies could maintain the current pace of AI infrastructure spending without pressuring cash flow.

The market became more selective. Companies involved in large-scale AI projects faced increased scrutiny, especially where spending plans outpaced near-term cash flow or relied on external financing like debt. Strong earnings and ambitious spending plans were no longer enough to push a company’s stock price higher, and sector leadership shifted toward firms demonstrating pricing power and a path to profitability. The changing AI narrative created periods of volatility and rotation within the tech sector, but it doesn’t necessarily mean the end of the AI trade. As with many transformative technologies, the initial excitement appears to be giving way to a focus on execution and profitability rather than broad enthusiasm and growth at any cost.

Equity Market Recap – Stock Market Ends the Year Near All-Time Highs

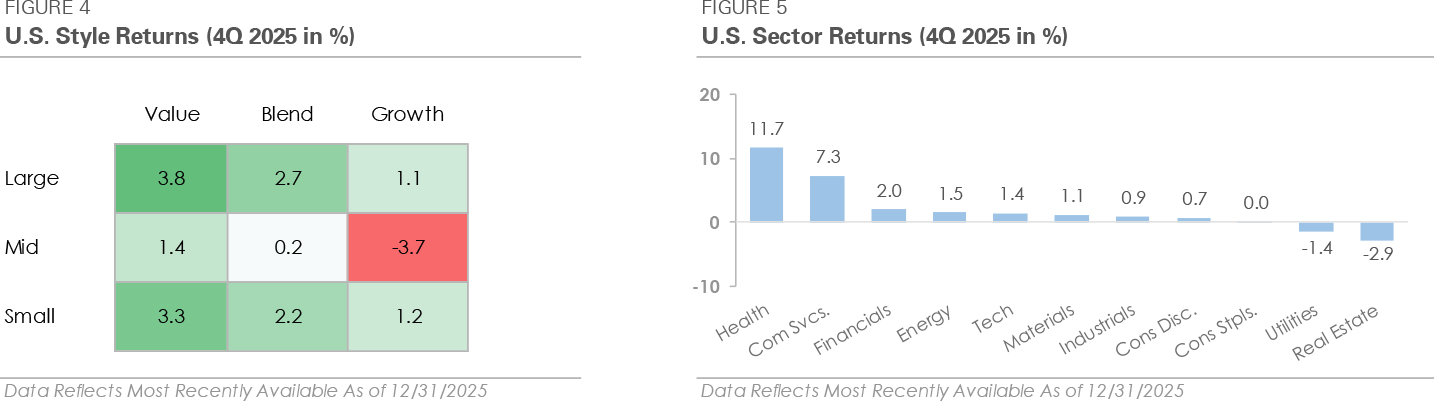

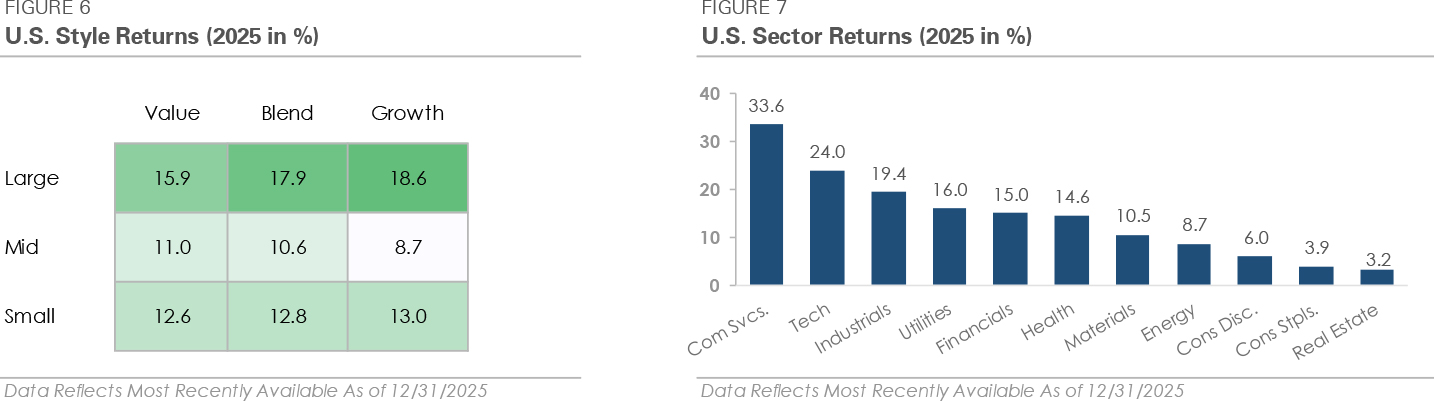

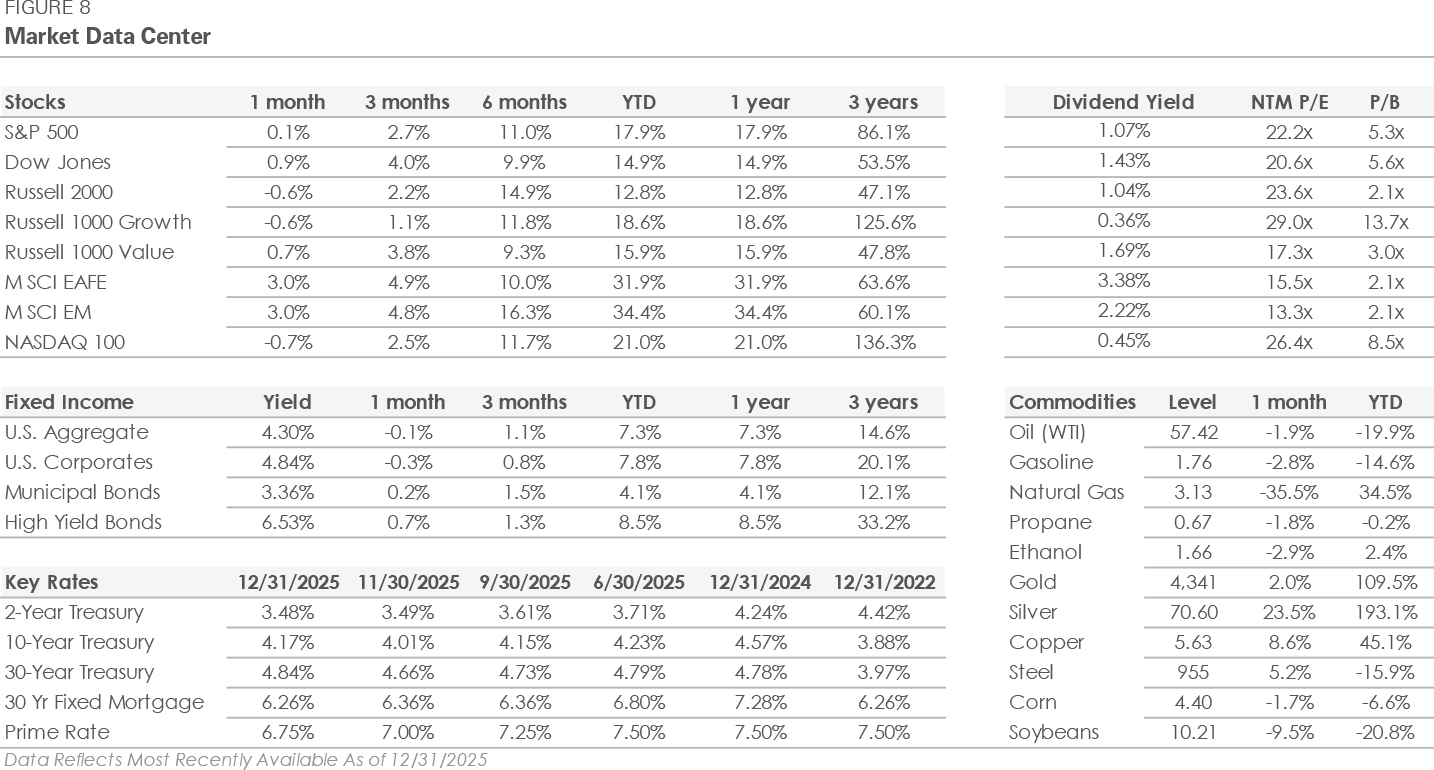

Stocks closed out the year with another quarter of gains, building on their momentum from earlier in the year. The S&P 500 gained +2.7% in Q4, bringing its year-to-date return to nearly +18%. The Nasdaq 100, an index of leading tech companies, gained +2.5%, raising its full-year return to +21%. Those headline returns were constructive, but the main development was a shift in market leadership. Large-cap value proxies led the market, with the Dow Jones Industrial Average and the Russell 1000 Value each gaining approximately +4.0%. The Russell 2000 gained +2.2%, with small-cap stocks rallying to new highs as the Fed cut twice.

Despite solid gains across the stock market, the pace of the rally continued to slow from the second and third quarters. Sector breadth also remained narrow, with only two S&P 500 sectors outperforming the broader index. Health care was the top-performing sector, benefiting from renewed interest amid increased AI scrutiny and a pause in tech leadership. The sector’s defensiveness and improved earnings stability were catalysts, but the quarter wasn’t defined by a flight to safety. The defensive trio of real estate, utilities, and consumer staples were the weakest sectors, signaling limited investor concern about the economy.

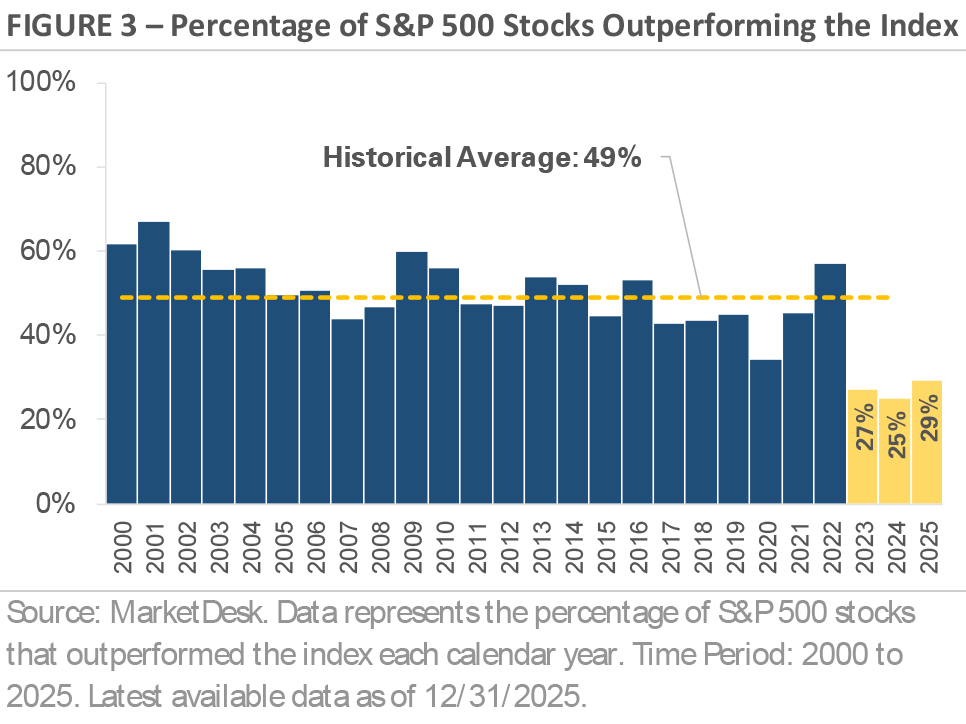

The shift in market leadership was modest, but it was notable. As shown in Figure 3, the percentage of S&P 500 companies outperforming the index has hovered around 30% the past three years. Those are significantly below the historical average of 49% and the three lowest years since 2000, illustrating how a small group of stocks has driven the S&P 500’s gains. The Q4 rotation occurred as the Fed cut interest rates twice, a move that the market believes will ease pressure on companies. Meanwhile, the AI trade in the stock market is becoming more selective as it enters its fourth year. The combination of lower interest rates and increased AI scrutiny could create opportunities for new leadership. If more companies start to outperform, it will represent a significant trend change in the market.

International stocks continued to outperform U.S. stocks, extending their gains from earlier in the year. Both developed and emerging market indices gained nearly +5% in Q4. For the full year, they each gained over +30% and outperformed the S&P 500 by more than +13%. Their outperformance isn’t a case of U.S. weakness, with the S&P 500 gaining nearly +18%, but rather broad international strength. A weaker U.S. dollar played a significant role, with the softness driven by rising trade tensions, policy uncertainty, and a rotation toward international stocks.

Credit Market Recap – Bonds Trade Sideways

The bond market was relatively quiet in Q4. As discussed earlier, the focus centered around the Fed’s rate cut plans. Yields on shorter maturity U.S. Treasury bonds fell as the Fed cut twice, while longer maturity yields ended the quarter modestly higher as economic activity remained solid and inflation remained stuck near 3%. Overall, the bond market has transitioned from a source of volatility during the Fed’s 2022-2023 rate-hiking cycle to relative stability and a source of income in 2025. Changing rate cut expectations and economic uncertainty have triggered periodic volatility, but the overall path has been smoother.

Corporate bonds traded higher in Q4. Credit spreads widened during periods of stock market volatility, but the moves were orderly and short-lived. The investment-grade and high-yield bond markets showed few signs of stress, and default expectations remained low. Both investment-grade and high-yield gained roughly +1% for the quarter, capping off strong full-year returns of approximately +8%.

As the new year begins, credit spreads remain tight by historical standards. Investment-grade and high-yield spreads are at their tightest levels in decades, signaling investor confidence in corporate fundamentals and the economy. While spread tightening has supported corporate bond returns, it means valuations are no longer cheap. Corporate bonds offer compelling yields for income-focused investors, but they also come with important trade-offs. When spreads are this tight, there’s less margin of safety if earnings or economic growth disappoint. For investors, it’s important to balance the income potential with credit risk.

2026 Outlook – Market Strength Raises the Bar

Before we turn the page to 2026, it’s worth reflecting on a year that was both eventful and remarkably calm. The year began with the stock market hitting new highs in February, only to reverse sharply as trade policy uncertainty triggered a nearly -20% sell-off. However, the sell-off set the stage for one of the strongest recoveries in decades. Fueled by AI enthusiasm, rate cut expectations, strong corporate earnings, and resilient economic growth, the S&P 500 set more than 35 new highs through year-end.

The S&P 500 finished 2025 with a nearly +18% gain, its third consecutive year of double-digit gains. It’s been an impressive run that included a global pandemic, aggressive rate hikes, and the rise of AI. Through it all, the stock market’s gains have been supported by solid economic growth and strong corporate earnings. Looking ahead, the bar is now higher. Today’s starting point is very different than a few years ago, or even last year. Stock valuations are more expensive, credit spreads are near their tightest levels in decades, and expectations for earnings and economic growth are high. None of these are red flags on their own, but they frame a market that already prices in rate cuts, strong earnings, solid economic growth, and the AI industry’s growth. The combination doesn’t necessarily signal a stock market sell-off, but it leaves less room for positive surprises.

Despite the higher starting point, there are many positives. The tech sector is experiencing a wave of innovation not seen since the internet era of the late 1990s. Companies are generating record profits. The S&P 500’s earnings grew by double digits the past two years, with expectations for solid growth in 2026. Consumers, the engine of the U.S. economy, continue to spend. Interest rates are coming down, which could unlock economic activity that higher rates delayed the past few years. Financial markets are open and functioning, and there’s no clear sign of systemic stress.

As we turn the page to 2026, it’s important to keep the big picture in mind. Markets have delivered impressive returns over the past five years, but each year brings its own surprises. We can’t predict what lies ahead, but we believe a disciplined approach focused on long-term goals, diversification, and risk management is the best way to navigate the market. Our team will continue to closely monitor incoming economic data and evolving market trends to help ensure portfolios remain aligned with your long-term objectives, regardless of what the market does in the short term.

This Quarter in Numbers

Important Disclosures

Published by Market Desk Research and distributed by QuadCap Wealth Management, LLC.

This client letter is being furnished by QuadCap Wealth Management, LLC (“QuadCap”) on a confidential basis for the exclusive use of clients of QuadCap. and may not be disseminated, communicated, reproduced, redistributed or otherwise disclosed by the recipient to any other person without the prior written consent of QuadCap.

This document does not constitute an offer, solicitation or recommendation to sell or an offer to buy any securities, investment products or investment advisory services. Such an offer may only be made to prospective investors by means of delivery of an investment advisory agreement, subscription agreement and other similar materials that contain a description of the material terms relating to such investment, investment strategy or service. This presentation is being provided for general informational purposes only.

This presentation includes information based on data found in independent industry publications and other sources and is current as of the date of this presentation. Although we believe that the data are reliable, we have not sought, nor have we received, permission from any third-party to include their information in this presentation. Charts, tables and graphs contained in this document are not intended to be used to assist the reader in determining which securities to buy or sell or when to buy or sell securities. Opinions, estimates, and projections constitute the current judgment of QuadCap and are subject to change without notice.

References to any indices are for informational and general comparative purposes only. There are significant differences between such indices and the investment programs described in this presentation. References to indices do not suggest that the investment programs will, or are likely to, achieve returns, volatility, or other results similar to such indices. The performance data of various indices presented herein was current as of the date of the presentation.

Past performance is not indicative of future results and there can be no assurance that the future performance of any specific investment or investment strategy will be profitable or equal any corresponding index or benchmark. The performance information shown herein is based on total returns with dividends reinvested and does not reflect the deduction of advisory and/or other fees normally incurred in the management of a portfolio. Stock performance and fundamental data is based on the following instruments: SPDR S&P 500 ETF (SPY), SPDR Dow Jones ETF (DIA), iShares Russell 2000 ETF (IWM), iShares Russell 1000 Growth ETF (IWF), iShares Russell 1000 Value ETF (IWD), iShares MSCI EAFE ETF (EFA), iShares MSCI Emerging Markets ETF (EEM), Invesco QQQ Trust (QQQ). Fixed Income performance is based on the following instruments: iShares Core U.S. Aggregate Bond ETF (AGG), iShares Investment Grade Corporate ETF (LQD), iShares National Muni Bond ETF (MUB), iShares High Yield Corporate ETF (HYG). Fixed Income yields and key rates are based on the following instruments: Bloomberg US Aggregate, ICE BofA US Corporate, ICE BofA US Municipal Securities, ICE BofA US High Yield, 2 Year US Benchmark Bond, 10 Year US Benchmark Bond, 30 Year US Benchmark Bond, 30 Year US Fixed Mortgage Rate, US Prime Rate. Commodity prices are based on the following instruments: Crude Oil WTI (NYM $/bbl), Gasoline Regular U.S. Gulf Coast ($/gal), Natural Gas (NYM $/mmbtu), Propane (NYM $/gal), Ethanol (CRB $/gallon), Gold (NYM $/ozt), Silver (NYM $/ozt), Copper NYMEX ($/lb), U.S. Midwest Domestic Hot-Rolled Coil Steel (NYM $/st), Corn (CBT $/bu), Soybeans (Chicago $/bu). U.S. Style performance is based on the following instruments: iShares Russell 1000 Value ETF (IWD), SPDR S&P 500 ETF Trust (SPY), iShares Russell 1000 Growth ETF (IWF), iShares Russell Mid-Cap Value ETF (IWS), iShares Russell Midcap ETF (IWR), iShares Russell Mid-Cap Growth ETF (IWP), iShares Russell 2000 Value ETF (IWN), iShares Russell 2000 ETF (IWM), iShares Russell 2000 Growth ETF (IWO). U.S. Sector performance is based on the following instruments: Consumer Discretionary Sector SPDR ETF (XLY), Consumer Staples Sector SPDR ETF (XLP), Energy Sector SPDR ETF (XLE), Financial Sector SPDR ETF (XLF), Health Care Sector SPDR ETF (XLV), Industrial Sector SPDR ETF (XLI), Materials Sector SPDR ETF (XLB), Technology Sector SPDR ETF (XLK), Communication Services Sector SPDR ETF (XLC), Utilities Sector SPDR ETF (XLU), Real Estate Sector SPDR ETF (XLRE).

Advisory Services are offered through QuadCap, an SEC registered investment advisor. QuadCap only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration is not an endorsement of the firm by the Commission and does not mean that QuadCap has attained a specific level of skill or ability.

The S&P 500 Index or Standard & Poor’s 500 Index is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.

The Russell 2000 index measures the performance of approximately 2,000 small-cap US equities.

The MSCI EAFE Index is a stock market index that measures the performance of large- and mid-cap companies across 21 developed markets countries around the world. Canada and the USA are not included.

The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries.

The Nasdaq 100 Index is a stock index of the 100 largest companies by modified market capitalization trading on Nasdaq exchanges.

The Russell 1000 Growth index is an index that tracks large cap, growth stocks. This benchmark is important for investors that might tilt their investments towards large cap growth. Growth stocks, in comparison to value stocks, are considered companies with a more growth potential, and a higher risk profile.

The Russell 1000 Value index is an index that tracks large cap, value stocks. This benchmark is important for investors that might tilt their investments towards large cap value. Value stocks, in comparison to growth stocks, are considered companies with a stable cash flow, and more mature business model.

The Dow Jones Industrial Average, or simply the Dow, is a stock market index that indicates the value of 30 large, publicly owned companies based in the United States, and how they have traded in the stock market during various periods of time. These 30 companies are also included in the S&P 500 Index. The value of the Dow is not a weighted arithmetic mean and does not represent its component companies’ market capitalization, but rather the sum of the price of one share of stock for each component company. The sum is corrected by a factor which changes whenever one of the component stocks has a stock split or stock dividend, so as to generate a consistent value for the index.

The Bloomberg US Aggregate Bond Index is used as a benchmark for investment grade bonds within the United States. This index is important as a benchmark for someone wanting to track their fixed income asset allocation.

The Bloomberg US Corporate Index covers performance for United States corporate bonds. This index serves as an important benchmark for portfolios that include exposure to investment grade corporate bonds.

The Bloomberg US Corporate High Yield Index covers performance for United States high yield corporate bonds. This index serves as an important benchmark for portfolios that include exposure to riskier corporate bonds that might not necessarily be investment grade.

Treasuries, also known as Treasury securities, are debt obligations issued by the United States government. They are used to raise cash needed to fund government operations and help finance the federal deficit. Treasuries are backed by the full faith and credit of the US government, making them one of the safest investments. They are an important instrument in monetary policy, allowing central banks to control the money supply.

The Prime Rate is the interest rate that commercial banks charge their most creditworthy corporate customers. The prime rate is derived from the federal funds rate, usually using fed funds + 3 as the formula.